Running a beauty salon means juggling a million things. You're managing your team, keeping clients happy, ordering supplies, fixing that wobbly styling chair, and somehow staying on top of color trends. Money talk? Yeah, that gets pushed to the bottom.

But then reality hits:

Sound familiar?

Here's the thing: salon funding isn't just for struggling salons. Even thriving businesses need capital to grow. Whether you want to upgrade equipment, hire that talented stylist, expand to a bigger space, or just sleep better during slow weeks, salon financing can change everything.

And honestly? Getting a loan for a beauty salon is way less scary than you think. You don't need perfect credit. Yes, there's paperwork, but it's manageable. In this guide, we'll walk you through exactly how to get a loan for a beauty salon, and we'll give you the real talk on beauty salon financing.

Let's get real for a second. Salon ownership is expensive. Like, really expensive. The beauty industry pulls in over $156 billion annually, with millions of salons competing globally. That's a huge market, which also means intense competition. To stay ahead, you need to constantly invest.

Picture this: A regular client sits down in your styling chair, and it makes that embarrassing squeaking sound. Again. Your blow dryers are so loud you practically have to shout over them.

Or maybe you're the opposite problem: business is booming, but you're maxed out. You had to turn away three people this week because your schedule is packed and you don't have another stylist to handle the overflow. That's not just frustrating, that's money walking out the door.

Bottom line? Salon funding isn't about desperation. It's about being smart and giving yourself resources to make people feel gorgeous.

Finding the right source to fund your salon business depends on your current situation. Here's where to start:

Okay, so not all salon loans are the same. Some are great for certain situations, others not so much. What works for you depends on how much money you need, how fast you need it, what your credit looks like, and what you're planning to do with it. Let's break it down without the finance jargon.

If you've looked into small business loans, you've heard about SBA loans. They're kind of a big deal. The Small Business Administration doesn't give you money directly. They tell banks, "We'll back you on this," which makes banks way more willing to say yes.

This is the popular one. You can use it for pretty much anything legit: new equipment, inventory, covering expenses, refinancing bad debt, or buying another salon.

Why people love them: Borrow up to $5 million (though most need way less), lower interest rates than regular bank loans, longer payback periods (10 years for most things, 25 for property), and smaller down payments.

The not-so-fun part? Weeks or months for approval. You'll need good credit, usually 680 or higher, to be competitive. But if you've got it and can wait, it's often worth it.

Same concept, faster. Max $500,000, approved in about 36 hours.SBA Express lets lenders approve you directly without waiting for SBA review, which speeds things up. The catch is that the SBA only guarantees 50% instead of the usual 75-85%, but you get your answer much faster.

The small ones: up to $50,000, averaging $13,000. Through nonprofit lenders who are more understanding if you're newer or building credit.

Got solid credit and a business that's been around for a bit? Traditional banks might give you better rates. But heads up: they're picky.

What they're looking for:

Term loans are straightforward: they give you money, and you pay it back over time. Business lines of credit are more flexible and, honestly, pretty handy. It's like a credit card for your business. You get approved for a certain amount, use what you need, and only pay interest on what you actually use. Super useful for those unpredictable months.

Equipment financing allows you to purchase business equipment by using the equipment itself as collateral. From a lender’s perspective, this significantly reduces risk: if repayments stop, the asset can be reclaimed. That is precisely why banks are often willing to finance 80–100% of the equipment’s cost, even for small or growing businesses.

Now, merchant cash advances (MCAs). These are the "I need money right now" option. You get cash within 24 to 48 hours, and the lender takes a percentage of your daily card sales until it's paid back. The upside? It's fast, and they don't care as much about credit. The payment adjusts to your sales, so slow days mean smaller payments.

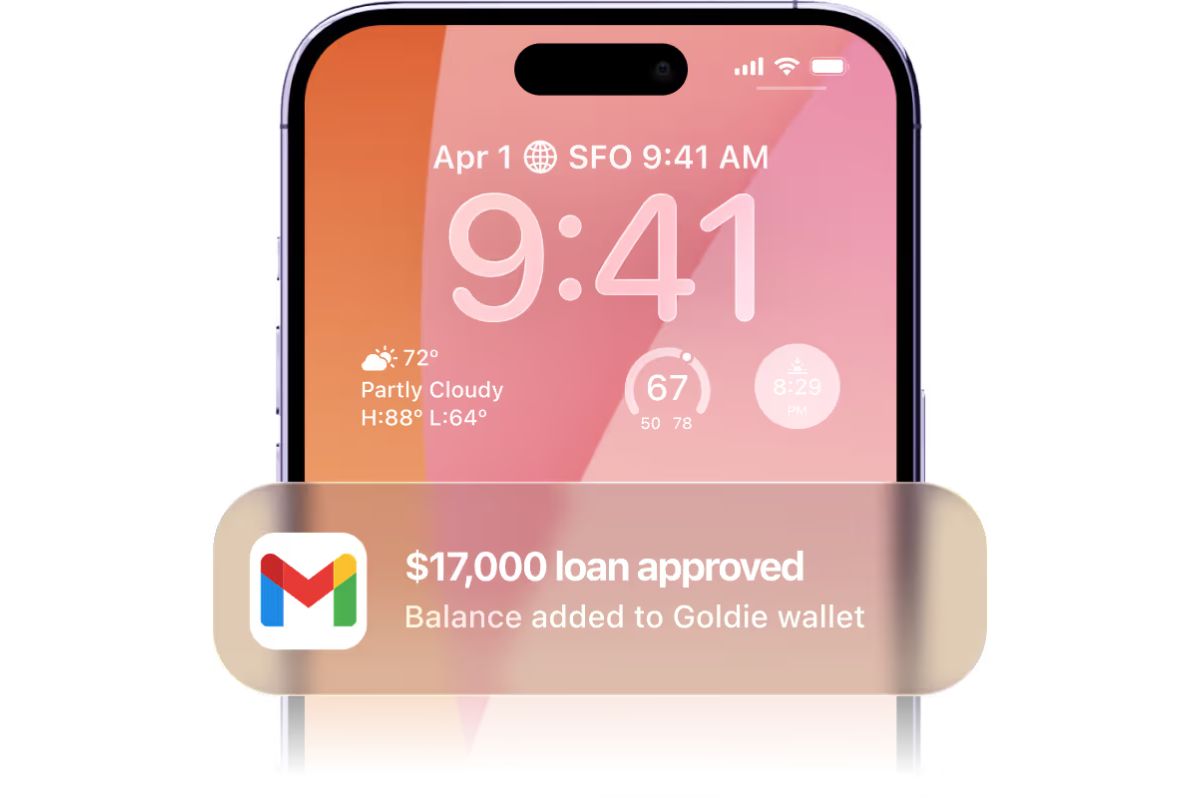

For beauty pros using Goldie, Stripe financing works the same way but is even simpler. You get quick access to funds with way less paperwork since they already see your revenue. It’s one flat fee with no interest or hidden charges. Repayment happens automatically based on your daily sales processed through the platform. No fixed monthly payments to stress about during slow seasons.

Identifying funding options for salon businesses is only the first step. Approval depends on whether you understand how lenders evaluate risk, and that’s where many applications quietly fail.

When assessing a beauty salon loan, lenders typically examine several core factors: your business’s financial stability, revenue consistency, credit history, time in operation, and the purpose of the loan. None of these exists in isolation. Together, they signal whether your salon can realistically service debt without strain.

Your credit score matters. Like, a lot. Here's the honest truth:

But listen: bad credit doesn't mean you're doomed. Plenty of salon owners with credit issues have gotten funding through SBA programs. They exist specifically to help small businesses that traditional banks won't touch.

Lenders want proof you're not going to disappear in three months. Traditional banks usually want at least two years of history. Alternative lenders might work with you after six to twelve months. Brand spanking new? SBA Microloans will give you a shot.

And yeah, you'll need to show them the money. Literally. Bank statements from the last three to six months, business tax returns (usually two years' worth), profit and loss statements, balance sheets, and cash flow projections. If your books are a disaster, fix them before you apply. Trust me on this. Organized financials make lenders way more comfortable saying yes.

For larger loans, lenders want a clear plan:

Your plan doesn't need to be 50 pages, but it should show you're strategic.

Some loans require collateral: assets the lender can take if things go south. This might include equipment, real estate, or personal assets.

You've decided to go for it. Good! Here's how it goes:

Okay, real talk time. This is the question that probably keeps you up at night. Taking on debt is scary. It's a big deal. And honestly? It's not always the right move. Let's figure out when salon financing actually makes sense versus when you should hit the brakes.

You have a clear ROI: That $5,000 balayage station lets you charge $50 more per service. Hiring a stylist costs $3,000 monthly but brings in $6,000. Do the math. If you'll make back way more than you're borrowing, that's smart.

You're bridging temporary gaps: January's dead after holidays. You know spring will be busy, but rent's due now. This is what short-term financing is for.

You're expanding strategically: Perfect second location available. Want to add lash extensions, and clients will book immediately. If the opportunity is real and you've done research, financing helps you move fast.

You can afford payments: Be honest. Can you make payments even in dead February? If payments will stress you out monthly, you're borrowing too much.

So, should you take a business loan to grow your salon? If you check these boxes above, the answer is probably yes.

You're covering ongoing losses: If your salon is losing money every single month, more debt isn't the fix. You've got deeper problems that need solving first. Loans should fuel growth, not keep a sinking ship floating for another few months.

You don't have a real plan: "I just need money" isn't a plan. Neither is "I'll figure it out later." Before deciding if you should take a business loan to grow your salon, you need to clearly explain what you'll do with the money and why it'll actually help your business. If you can't do that, wait until you can."

The terms smell fishy: If a lender is pushing you to sign RIGHT NOW, or the interest rate seems insane, or there are fees everywhere you look, walk away. Legitimate lenders give you time to think and don't use pressure tactics.

Your personal finances are unstable: Many business loans require personal guarantees. That means if your salon can't pay, they're coming after your personal stuff. Your credit, your house, your savings. Make sure you can handle that risk before you sign anything.

Here's good news: beauty salon financing has completely changed. Newer fintech companies offer approval and funding in one to two business days. No more weeks of waiting. This is what stress-free financing looks like in practice."

These programs work differently. Instead of just obsessing over credit scores, they look at your actual business performance. Your payment history, real sales numbers. They want to see how your business actually does.

What makes it different:

Platforms like Goldie even offer Stripe financing right through their software, which is convenient since they see your real-time sales data. With Stripe loans integrated into Goldie, you get fast access to capital without leaving your salon management platform.

Look, getting a loan for a beauty salon doesn't have to be terrifying. Yeah, there's paperwork. But here's the truth: with the right approach, salon funding can transform your business from barely hanging on to absolutely thriving.

Need new equipment? There's financing.

Want to hire that amazing stylist? There's financing.

Dreaming about a bigger space? There's financing.

Stressed about slow season? There's financing for that, too.

From government-backed SBA loans (lowest rates, need patience) to fast merchant cash advances (quick money, flexible repayment), you've got real options.

Here's the thing: you opened a salon because you're passionate about making people feel confident and beautiful. With the right financing partner and a clear plan, there's no ceiling on what you can build.

Still asking yourself if you should take a business loan to grow your salon? Take that first step today. Future you will be so grateful!

.webp)